Traditional liquidity risk measures like Basel III are too static to detect emerging threats in real time, as demonstrated by crises from 2008 to COVID-19. This blog presents the Bank of Tanzania’s machine learning-based Bank Liquidity Risk Supervision (BLRS) solution, which can retrain and predict liquidity risk classifications in under two minutes.

Author: Rweyemamu Barongo, Head, AI & Data Innovation Hub, Bank of Tanzania

This article represents the author’s personal perspectives based on research conducted during the Innovation Leaders Residency initiative.

_______________________

Introduction

Post-COVID interest hikes increased debt-servicing costs, reduced consumer spending, and escalated defaults, straining banks’ liquidity positions. These shifts underscore the need for more adaptive and precise liquidity risk supervision. While traditional liquidity adequacy measures and those proposed by Basel III remain bound by static data and rigid assumptions, machine learning offers the flexibility needed to rapidly respond to emerging liquidity threats in real time. The Bank of Tanzania (BOT), with mentorship from the Cambridge SupTech Lab, innovated a Bank Liquidity Risk Supervision (BLRS) solution to complement traditional supervision methods. Initial tests of the solution indicated improvement in model retraining speed and prediction accuracy previously unattainable for data-driven financial supervision.

Context and Challenges

Traditional adequacy measures of liquidity risk, such as the Minimum Liquid Assets requirements (MLA), overemphasise ratio compliance but are too slow to detect liquidity risk and exposures. In 2008, numerous banks using traditional liquidity risk compliance ratios failed to detect severe liquidity shortages until it was too late, leading to financial institution failures and a Global Financial Crisis. Thus, the Basel Committee on Banking Supervision (BCBS) introduced Basel III standard adequacy measures in 2009: the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). Basel III addressed liquidity measures’ limitations on detecting liquidity risk quality and stability, including the provision of critical liquidity buffers. However, only 21% of financial jurisdictions managed to transition to Basel III by 2021 due to complex Basel III reporting requirements. Basel III measures are also static, relying on past data and unable to react quickly to sudden shifts in market conditions, resulting in delayed regulatory responses. They could not foresee and respond to real-time disruptions like the COVID-19 market shocks. The sudden economic shutdowns resulting from the pandemic led to rapid business and household revenue declines, increasing liquidity demands on banks. Basel III is also inadequate to provide insights into the underlying health of a bank’s assets and funding sources, and their sufficiency relative to market dynamics. FED post on 30 April 2021 indicated liquidity shocks in Wells Fargo, Morgan Stanley, and Goldman Sachs despite a good LCR above 100%. This for underscores the need for more dynamic tools. BLRS applies Machine Learning estimations that were proven to improve out-of-sample prediction performance and provides better early warning tools. BLRS is anticipated to provide timely identification of emerging risks for quicker interventions.

Research and Methodology

The BLRS adopted a Hybrid Machine Learning (HML) model from Barongo & Mbelwa’s (2023). HML is a hybrid of 199-tree Random Forest (RF) and 10-512-250-120-80-60-6 Multi-Layer Perceptron (MLP) supervised classification models. It uses data from 10 variables on banks’ funding and asset allocation strategies, quality of credit portfolio, and macroeconomic performance. Labels were the liquidity risk classes 1-to-5, representing strong to critically deficient liquidity risk positions. All data were sourced from the BOT. HML prediction benchmarking with related studies indicated superior statistical performance in Accuracy, Balanced Accuracy, Precision, Recall, F1 Score, G-mean, Cohen’s Kappa, Youden Index, and Area Under the Curve. Further, HML demonstrated the detection of hidden patterns of used variables in non-linear data, allowing for more accurate HML risk detection than MLA traditional measures that rely on linear assumptions. The HML model excels at detecting hidden patterns that are difficult for MLA to recognise. Practical benchmarking of HML with MLA traditional liquidity classification, using past data, indicated better HML performance than MLA in earlier detection of liquidity risk. HML also demonstrated superior performance in imbalanced datasets, thanks to advanced data science techniques. HML retraining was 120 seconds, which enables a 2-minute near real-time prediction by HML and indicates suitability to adjust to market dynamics unlike Basel III measures.

Solution Overview

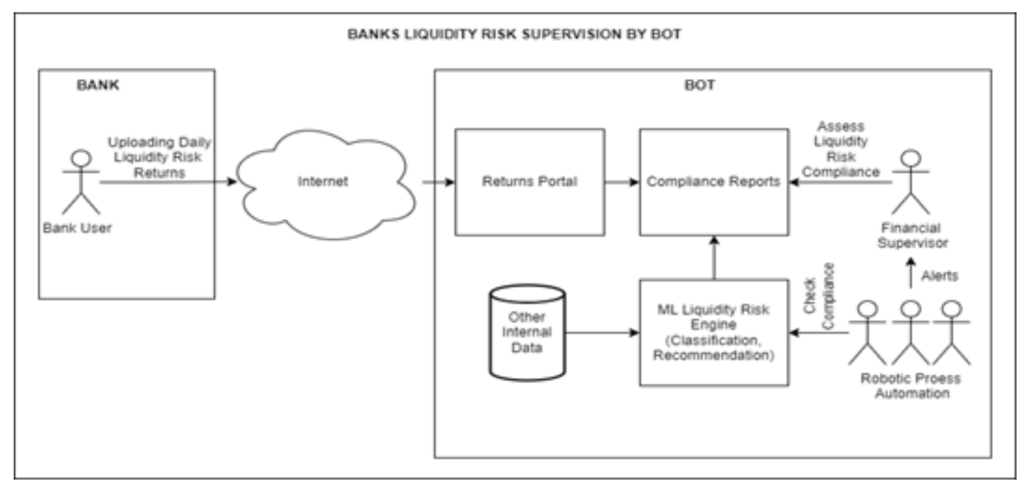

The BLRS solution in Figure 1 is under implementation at BOT to enhance liquidity risk supervision using a machine learning approach. It is implemented as an in-house innovation task by the collaboration of IT and business experts. Once data is submitted via API or spreadsheets, BLRS immediately processes it through a Big Data platform, allowing it to analyse thousands of data points in seconds, considering macroeconomic data and liquidity risk labels. This enables regulators to identify and respond to potential liquidity risks within two minutes of data updates, a significant improvement over the previous intervention delay of a day or more. These returns include critical data such as liquidity ratios, funding strategies, and market performance metrics. The machine learning model is trained to detect patterns that may indicate emerging liquidity threats by analysing liquidity risk factors, such as potential shortfalls or vulnerabilities that could go unnoticed by traditional supervision methods. With BLRS, regulators can receive alerts within minutes of emerging liquidity threats, enabling them to intervene before a crisis unfolds, preventing the escalation of risks that could have previously gone undetected. In mid-2025, the tool is set to incorporate Robotic Process Automation (RPA) and a recommendation system, which will further streamline the supervision process. For example, when a bank’s liquidity ratio dips below a critical threshold, BLRS will trigger automated alerts and recommend corrective actions in real time, reducing the manual monitoring efforts and response time for regulatory intervention.

Figure 1: BOT BLRS architecture for Liquidity Risk Detection

Evaluation

BLRS will be evaluated on the accuracy and explainability of results and the ability to adapt to new data within two minutes or less for model retraining. Model training and tests will be evaluated by benchmarking with HML results in the paper. Adverse training and test statistics will require machine learning re-engineering. Prediction performance will involve the practical performance test on how well the tool works in real-life situations and the statistical performance test to measure its accuracy through various data benchmarks. The practical test will involve comparative analysis versus traditional measures and actual liquidity risk position. A parallel report on factor analysis will enable regulators to see exactly how the model arrived at its decisions, proving transparency, clear accountability and reducing the risks of biases going unchecked. Statistical performance will benchmark BLRS versus HML in statistical metrics from the paper. The adverse practical or statistical performance will require BLRS improvements.

Anticipated Impact

The anticipated impact is substantial: BLRS will reduce false regulatory alarms while accurately predicting actual liquidity threats, providing a more reliable foundation for decision-making, while banks benefit from more targeted and timely interventions, ultimately contributing to greater financial stability in the banking sector. In the day-to-day operations, RPA will ease repetitive checks for liquidity compliance and enable the dedication of resources to other analyses.

AI Ethics and Challenges

Ethics in financial supervision is crucial to ensure fairness, transparency, and accountability. It helps prevent conflicts of interest, promotes trust in regulatory institutions, and guards against potential biases in decision-making. In AI-driven liquidity risk supervision, like the BLRS model, ethical governance ensures that decisions are unbiased, prevents disproportionate impacts on smaller banks, and maintains transparency, especially when machine learning models influence critical financial stability interventions. AI ethics and governance considerations at BOT will be guided by the BOT AI Adoption Strategy, which is under discussion. In a pilot test, BOT will conduct regular reviews of the model outputs to ensure that predictions do not disproportionately impact smaller banks, preventing skewed results that could unfairly penalise certain institutions. Data are anonymised and standardised upon ingestion for model development.

Liquidity data is imbalanced with a 4% occurrence of liquidity risk incidents, risking data bias. To tackle data bias, BLRS is implementing a data vetting process, utilisation of a diverse dataset, and regular audits of the model’s performance, ensuring that predictions are not skewed by any single dataset. Additionally, analysis of factors along with BLRS liquidity reports will provide transparency by allowing the regulator to trace how the model reached each decision, further reducing the risk of bias and its significance for AI explainability. The selection of a hybrid model generalises prediction and reduces model biases. This strategy will allow addressing potential biases and ensure that the AI tool remains a fair and effective resource for prudential supervision.

Conclusion

As AI continues to advance, its ability to anticipate and manage risks will not only make individual institutions more secure but also protect the global financial system from the kinds of shocks that have caused major crises in the past.

_________________

For further information, we encourage you to read the State of SupTech Report 2025, access session recordings and engage in discussions on GovSpace.io.