As the insurance industry undergoes rapid digital transformation, supervisors must evolve beyond traditional methods to embrace data-driven, AI-powered tools. This blog explores how SupTech solutions — from NLP-based market monitoring to automated underwriting review — are reshaping insurance supervision globally, with examples from MAS, the ECB, and France’s ACPR.

Author: Laura Lopez Maldonado, Chief, Insurance Supervision Department, Superintendencia de Banca, Seguros y AFP del Perú

This article represents the author’s personal perspectives based on research conducted during the Innovation Leaders Residency initiative.

_________________________

The New Insurance Supervisor

Insurance supervisors have played a fundamental role in safeguarding the solvency of the insurance system and maintaining proper market conduct to ensure market stability and protect policyholders. This work has demanded significant effort and expertise. Through regulation and the review of extensive information such as financial statements, regulatory reports, insurance contracts and claims data, supervisors have implemented corrective actions to ensure the entities fulfill their contractual obligations, act with transparency, and treat consumers fairly.

In this context, the rapid digital transformation presents an opportunity to significantly enhance the supervisory work. To make use of the increasing availability of data and the potential of emerging technologies, supervisors must develop new skills, knowledge, and tools to stay ahead of ongoing changes in the insurance industry and consumer behaviour. This evolution enables a more comprehensive analysis of process changes and emerging risks across the insurance value chain. In this sense, data analytics, cybersecurity, data governance and personal data protection expertise have become increasingly relevant.

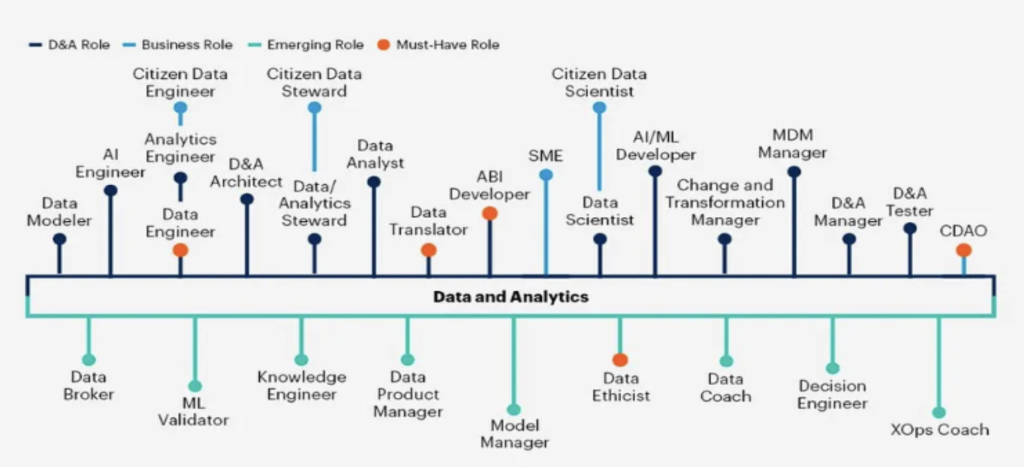

This shift does not replace supervisors’ experience. However, it complements it with tools that automate manual processes, leverage non-traditional information sources such as social media and unstructured data, and utilise artificial intelligence (AI) for assistant functions. Technologies like machine learning, deep learning, natural language processing (NLP), and large language models (LLM) play a crucial role in this transformation. Furthermore, as highlighted by Gartner in 2022, new roles and functions are emerging within organisations as part of their digital transformation – including supervisory and regulatory authorities, which are undergoing a transition towards becoming data-driven institutions.

Figure 1: The emerging spectrum of data and analytics roles – Source: Gartner (2022)

Changes in the Insurance Industry

Understanding the evolving role of insurance supervisors begins with an analysis of the insurance industry itself. According to Junguito (2008), this industry dates back approximately 2,000 BCE when Babylonian merchants collectively covered losses from damaged goods during transport or compensated families for losing a member. Over time, the industry has transformed significantly.

For instance, insurance companies were traditionally large physical entities investing heavily in infrastructure – such as branch offices, to reach customers. Today, technology has enabled these firms to operate without physical spaces, allowing closer customer engagement via websites, mobile apps, and social media platforms.

This technological shift has not only changed how insurance companies operate but also given rise to a new category of firms known as Insurtechs. According to the International Association of Insurance Supervisors (IAIS) in 2017, Insurtech refers to emerging insurance technologies and innovative business models with the potential to transform the insurance industry.

The insurtech ecosystem is diverse. It includes traditional insurers that incorporate technology into specific processes, fully digital startups offering innovative insurance solutions, technology providers known as BigTech, and innovation incubators, including universities – that serve as sources of knowledge and research.

Moreover, the digital transformation has not been limited to insurers alone. Other key market participants – insurance intermediaries, distributors, reinsurers, and policyholders – have also had to adapt to this new digital landscape.

Insurance intermediaries, including brokers, adjusters, and surveyors, have shifted from face-to-face advisory services and physical documentation to digital platforms, websites, and mobile applications for enhanced customer interaction and allow for faster, more efficient communication.

Reinsurers have also evolved. Operating on the principle of risk diversification across products, geographies, and economic sectors, they now rely heavily on advanced analytics and predictive modelling to assess market behaviour, identify opportunities, and manage risk exposure more efficiently. With access to vast amounts of data form multiple sources – such as underwriting information, natural catastrophe models, economic indicators, climate data, and even satellite imagery – reinsurers are increasingly using AI and machine learning algorithms to improve risk assessment, pricing and capital allocation.

Another key aspect is the new profile of insurance consumers, whose habits and behaviours have evolved. Today’s consumers seek personalised products tailored to their specific needs and want to acquire them quickly and easily, often avoiding complex or lengthy physical contracts. These new consumers are far more informed and can easily compare prices and conditions. Additionally, they are highly connected to information circulating on the internet and social media platforms, trusting the messages they hear and see there.

Considering these profound transformations across the insurance value chain, it becomes evident that supervisors must also evolve. Supervisors are now expected to assess how digital transformation impacts not only existing regulations but also supervisory processes, to make them more efficient, risk-based, and data-driven.

New regulatory frameworks may be required to address several emerging issues. These include updating rules for digital distribution and onboarding, setting standards for electronic policies and digital signatures, and strengthening cybersecurity and data governance frameworks. Additionally, supervisors may need to regulate outsourcing to technology providers, ensure the ethical use of AI in underwriting and claims, and promote digital financial inclusion while preventing algorithmic bias or exclusion.

Changes in the Insurance Value Chain

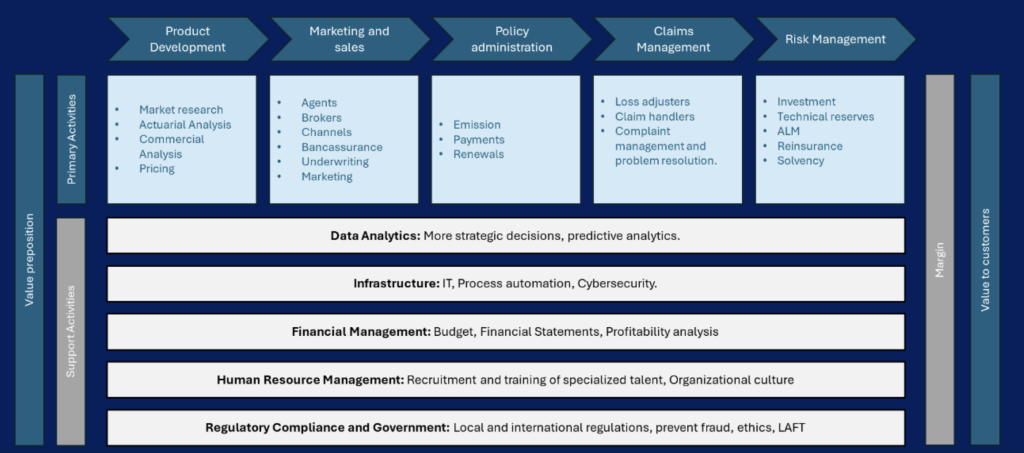

Another way to understand the evolving needs of insurance supervisors is by analysing how technology is being integrated across the insurance value chain. This value chain comprises primary and support activities (See Figure 2).

Primary activities include product development, marketing and sales, policy administration, claims management, and risk management. Support activities include data analysis, infrastructure, financial management, human resources, corporate governance, and regulatory compliance.

Figure 2: Value Chain of an Insurance Company – Source: Own Elaboration

In product development, AI is leveraged to design innovative insurance solutions, while advanced data analytics enables dynamic and personalised pricing. Insurers can now tailor pricing structures to different segments, improving both risk selection and product adequacy – by analysing customer specific characteristics such as habits, lifestyles, and risk profiles.

In distribution and sales, AI-driven tools enhance customer experience, refine product offerings, and optimise marketing strategies. Chatbots and virtual assistants now provide 24/7 support, respond to queries, generate personalised quotes, and guide clients through the purchasing process. Additionally, big data analytics allows for more precise customer segmentation, enabling targeted marketing campaigns that reduce acquisition costs. Predictive analytics supports customer retention by identifying behavioural patterns that signal renewal needs or cancellation risks, allowing for timely interventions.

Policy administration has been significantly streamlined through technology, improving both operational efficiency and customer satisfaction. AI-powered underwriting automates risk assessment and eligibility determination, reducing manual errors and expediting policy issuance. Online platforms now allow customers to input personal information and automatically receive their policies upon validation. Electronic signatures also facilitate seamless policy issuance with full legal validity. Payment flexibility has also expanded, with policyholders able to make premium payments through credit and debit cards, mobile wallets, direct bank transfers, and even cryptocurrencies. Finally, automated systems can track policy expiration and trigger renewal processes with minimal human intervention.

Claims management has transformed, and the digitalisation has brought notable improvements in efficiency, fraud prevention, and customer experience. Policyholders can now submit claims through digital portals, mobile applications, or chatbots. These platforms guide users step-by-step, through the claims process, ensuring accurate submission of required documents. AI tools are increasingly used to analyse photos, videos and documentation to determine claim validity and estimate compensation amounts. Machine Learning algorithms also detect patterns indicative of fraud, allowing insurers to identify anomalies and prevent false claims, ultimately reducing financial losses.

Finally, risk management has evolved with technological advancements, empowering insurers to assess, predict, and mitigate risks more precisely. Sophisticated algorithms analyse market trends, economic data, and portfolio performance to support informed decision-making. Advanced software facilitates accurate reserve calculations, while machine learning models predict future claims patterns and forecast future cash flows. Monte Carlo simulations allow insurers to evaluate a wide range of scenarios and their impact on investments, reserves, risks exposure and solvency.

International experiences

Monetary Authority of Singapore (MAS)

The Monetary Authority of Singapore (MAS), the financial regulator of Singapore, is a notable example of the success of prudential supervision, as documented by the Financial Stability Institute (FSI, 2022).

For prudential supervision, MAS has developed a network analysis tool to map interconnections between insurance companies and reinsurers. This tool employs graph visualisation and pattern recognition algorithms to identify risk transfers and exposures across insurers and reinsurers, thus detecting concentration risks within the insurance industry. For instance, multiple insurers may cede risks to the same reinsurer, creating a systemic dependency. If the reinsurer experiences financial distress, it could significantly impact the ceding insurers. The tool allows regulators to identify such interconnections, assess the systemic importance of reinsurers, and design stress test scenarios for the industry. It also provides insights into specific business lines, types of reinsurers, cession ratios, and recoverable amounts.

In the area of anti-money laundering and countering the financing of terrorism (AML/CFT), as documented by the Financial Stability Board (FSB, 2020), MAS has taken a proactive approach by integrating advanced analytics, automation, and cross-agency collaboration. MAS has developed tools that apply machine learning algorithms to transaction data and customer profiles to detect unusual behaviour and identify hidden patterns indicative of illicit activity. These tools are capable of generating real-time alerts, which can be further investigated by supervisory teams or shared with relevant enforcement authorities.

MAS has developed a tool that applies text analysis techniques to the audited financial statements of supervised institutions, enabling the identification of key words that may signal potential risks. Combined with financial metrics and visualised through an automated dashboard, this tool has enhanced the efficiency of report reviews.

MAS also uses AI tools to identify harmful financial practices, including mis-selling investment and insurance products. Additionally, it uses NLP to analyse vast amounts of unstructured data, including regulatory reports submitted to the supervisor, enabling the identification of areas that require supervisory attention. NLP has also been leveraged to monitor social media and news outlets, helping to identify early warning signals or developing stories that may require proactive supervisory action.

French Prudential Supervision and Resolution Authority (ACPR)

As highlighted by the Financial Stability Institute (FSI, 2022) in relation to market conduct, the French Prudential Supervision and Resolution Authority (ACPR) is developing a speech-to-text automation tool to transcribe recordings of insurance marketing phone calls between insurance agents and customers.

To ensure compliance with insurance distribution regulations, supervisors currently listen to and transcribe these recordings manually. ACPR is developing a machine learning – based tool using pre-trained, open-source models to automate this manual process. All data is stored on a local server, with multiple security measures in place to safeguard personal information. If sensitive data is shared during conversations, a dedicated process removes such information once the supervisory review is completed. Future enhancements to the tool may include NLP algorithms capable of identifying unfair business practices or detecting missing mandatory terms within transcribed conversations.

European Central Bank

The European Central Bank (ECB) has made suptech a strategic priority in its vision for banking supervision by establishing a dedicated SupTech Hub and launching a Digitalisation Roadmap (FSI, 2023).

The ECB is developing the SupTech Virtual Lab, a cloud-based platform designed to enable secure and remote collaboration across the Single Supervisory Mechanism. As part of its hub-and-spoke innovation model, the Virtual Lab will allow supervisors to co-develop and share Python and R models, connect to centralised data sources, access shared microservices, and participate in training and joint projects. Featuring interactive notebooks, the platform enhances transparency in data analysis and supports advanced AI and machine learning needs through scalable infrastructure. It also integrates best practices in software development, including version control and model governance. Overall, the Virtual Lab aims to foster an inclusive, data-driven supervisory culture across the Eurosystem.

Furthermore, the ECB has developed a tool using Natural Language Processing (NLP) and Machine Learning (ML) to partially automate the review of Fit and Proper questionnaires, which are currently processed manually in various formats and languages. The tool translates and digitises the information, flags potential concerns, and stores the data for future analysis. A 2020 proof-of-concept demonstrated its effectiveness, though challenges remain with scanned documents. The tool is expected to save case handlers significant time and improve over time through user feedback. Its secure, modular architecture also allows for flexible application to other supervisory processes.

Benefits, Risks and Preconditions of Implementing Suptech Solutions

Implementing suptech solutions offers several advantages, including enhanced data-driven decision-making by automating information collection and analysis from insurers. Continuous monitoring enables early detection of irregularities while optimising regulatory compliance processes. Additionally, it facilitates the deployment of early warning systems to identify financial risks, strengthens risk assessment through simulations and advanced analytics, improves operational efficiency by reducing manual supervisory workload, and minimises the risk of human error by automating key processes.

However, suptech also presents challenges such as over-reliance on technology, rapid technological obsolescence, complexity and high implementation costs, resistance to change, and cybersecurity risks. To mitigate these risks, regulators must adopt strategies that ensure a balanced use of technology, including scalability testing of solutions, and implementing advanced security measures.

The preconditions for developing suptech solutions and to have a strategy within an insurance supervisor encompass a wide range of organisational, technological, and cultural aspects. First, strong commitment from senior leadership is essential to position digital transformation as a strategic priority. A sound technological infrastructure is required, along with access to and adoption of emerging technologies that enable innovative supervisory tools. An organisational culture that embraces change, supported by flexible internal processes, is key to encouraging experimentation and ongoing adaptation. Data should be treated as a strategic asset, safeguarded by robust cybersecurity measures and personal data protection policies. Furthermore, international collaboration and cooperation with other supervisory authorities, industry associations, academic institutions, and multilateral organisations are vital. Talent development must also be prioritised through the identification of new roles and skillsets, as well as the recruitment and retention of personnel with expertise in data analysis, technology, and risk-based supervision. Together, these conditions provide an enabling environment for the successful implementation of a suptech strategy aligned with supervisory objectives.

Conclusions and Recommendations

In the face of an increasingly complex and digitalised insurance landscape, the integration of suptech solutions into supervisory practices is no longer optional – it is essential. The evolution of the insurance value chain, the emergence of new risks, and the growing expectations of digitally-savvy consumers all demand that supervisors modernise their approach.

Suptech offers the means to enhance data analysis, streamline operations, and respond to systemic risks in real-time, allowing for more agile, proactive, and risk-based supervision. Far from replacing human judgement, these technologies serve to complement and empower supervisory teams with richer insights, improved efficiency, and better-informed decision-making capabilities.

To ensure the successful adoption of suptech, it is imperative that insurance supervisors commit to a long-term, strategic transformation. This involves investing in digital infrastructure, cultivating an open and innovative organisational culture, and collaborating across borders and sectors.

Ultimately, suptech should be viewed not only as a set of tools, but as a catalyst for reshaping supervisory institutions into data-driven, forward-looking authorities capable of safeguarding market integrity in the digital age. The journey ahead requires vision, adaptability, and cooperation – but the potential rewards for supervisors, insurers, and policyholders alike are substantial.

References

- Financial Stability Institute (2022): “Suptech in insurance supervision”.

- Financial Stability Board (2020): “The Use of Supervisory and Regulatory Technology by Authorities and Regulated Institutions – Market developments and financial stability implications”.

- Financial Stability Institute. (2020). The SupTech Generational Shift – A report on the use of technology in supervision. Bank for International Settlements.

- Financial Stability Institute. (2023). Suptech use cases in prudential supervision: selected examples. FSI Insights on policy implementation No. 46.

- International Monetary Fund. (2019). Singapore: Technical Note on Fintech: Implications for the Regulation and Supervision of the Financial Sector. IMF Country Report No. 19/223.

- Cambridge SupTech Lab. (2024). In the SupTech Loop #9: GenAI, ESG data, and risk frameworks.

- Cambridge SupTech Lab. (2024). In the SupTech Loop #14: COSMIC and collaborative SupTech for AML.

- Deloitte. (2023). Riding the Disruptive Wave: How Regulators Are Dealing with Emerging Technologies in the Financial Sector.

- Monetary Authority of Singapore. (2022). Harnessing Technology for Supervision – MAS Annual Report 2021/22.

- European Insurance and Occupational Pensions Authority (EIOPA) (2023): “EIOPA´s Digital Strategy”.

- European Insurance and Occupational Pensions Authority (EIOPA) (2020): “Supervisory technology strategy”.

- International Association of Insurance Supervisors (IAIS) (2020): “Issues Paper on the Use of Big Data Analytics in Insurance”.

- Junguito, R. (2008). Reseña sobre la historia de los seguros. Revista Fasecolda, (128), 16-18.

- Simone di Castri, Matt Grasser, and Arend Kulenkampf. Regtech for Regulators Accelerator (2018): “Financial Authorities in the Era of Data Abundance RegTech for Regulators and SupTech Solutions”, August

- Cambridge SupTech Lab (2023), State of SupTech Report 2023, Cambridge: University of Cambridge. Available at www.cambridgesuptechlab.org/SOS.

- International Association of Insurance Supervisors (IAIS) (2018): “Issues Paper on Increasing Digitalisation in Insurance and its Potential Impact on Consumer Outcomes”.

- Oletzky, T., 2023. InsurTech in the United States and Germany—What are the drivers behind the different business models? Risk Management and Insurance Review, 26(4), pp.485-511. https://onlinelibrary.wiley.com/doi/pdf/10.1111/rmir.12254

- Oliva, F., & Flores, M. (2017). La transformación de las compañías de seguros en la era digital. Revista VisiónDeloitte.

- Ma, Z. and Liu, J., 2023, December. Research on Insurance Regulation under the Background of InsurTech. In 3rd International Conference on Digital Economy and Computer Application (DECA 2023) (pp. 126-132).

- Atlantis Press. https://www.atlantis-press.com/proceedings/deca23/125995017

- Morante, T.F. and Contreras, Y.R., 2020. Insurtech Regulatory Developments in Latin America. Business Law Today. https://businesslawtoday.org/2020/09/insurtech-regulatorydevelopments-latin-america/

- Marano, P. and Siri, M., 2021. Regulating insurtech in the European Union. https://www.um.edu.mt/library/oar/bitstream/123456789/109656/1/Regulating_insurtech_in_the _European_Union%282021%29.pdf

- McKinsey & Company, 2024. Global Insurance Report 2025: The pursuit of growth.

_________________________________

For further information, we encourage you to read the State of SupTech Report 2025, access session recordings and engage in discussions on GovSpace.io.